Each year we publish a Market Cleanliness (MC) Statistic for takeover announcements in the UK equity markets. This is defined as the proportion of corporate takeover events for which we observed a significant abnormal movement in share price before the takeover announcement.

Market Cleanliness (MC)

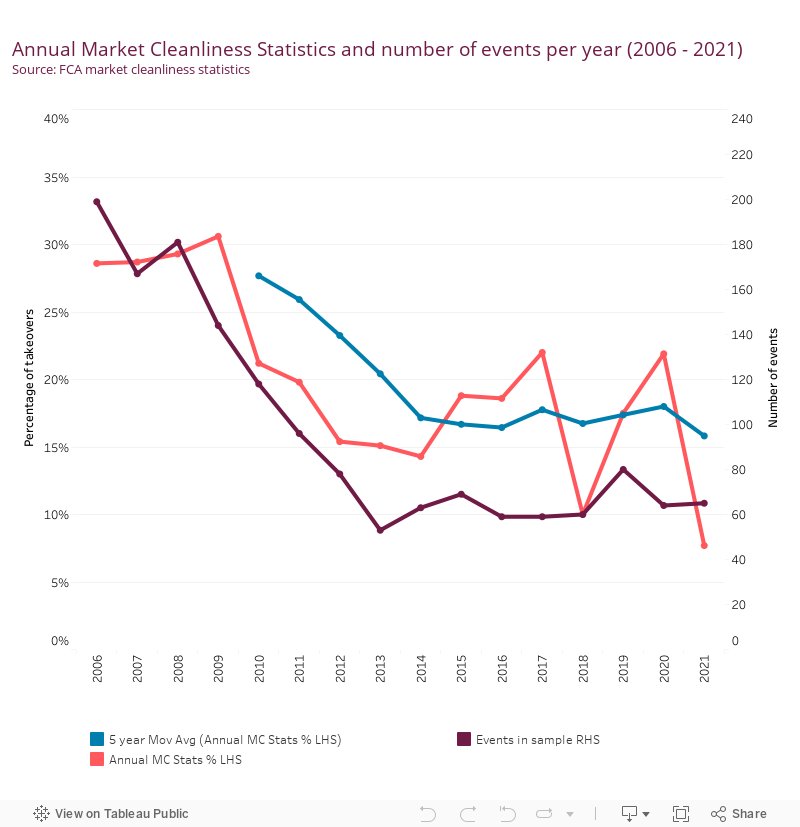

Figure 1: Annual Market Cleanliness Statistics and number of events per year (2006 – 2021)

The MC statistic for 2021 was 7.7%. This represents a reduction over the previous year, though it is difficult to draw meaningful conclusions from year-on-year changes. We therefore now calculate the 5-year moving average of the MC statistic to enable better interpretation.

The MC statistic is one indicator of possible insider dealing, but it has several shortcomings as a measure of broader market cleanliness, especially given the fall in the number of corporate takeover events over the past decade. The episode of high volatility after the Covid-19 shock in March 2020 could have had an impact on the recent levels of the MC Statistic. Potentially some pre-announcement price movements in 2021 might not have been identified as abnormal due to the periods of high volatility in the year before the announcement, which we use to assess the price movements’ statistical significance. Other factors can influence the statistic, such as financial analysts or the media correctly predicting likely takeover targets and this or other factors leading to significant legitimate trades ahead of an announcement. We also monitor a range of additional indicators.

Abnormal Trading Volume (ATV)

Each year we publish an Abnormal Trading Volume (ATV) Measure. This looks for abnormal increases in trading volumes ahead of potentially price sensitive announcements, covering equity instruments and some equity derivatives.

The ATV measure for 2021 was 7.1%. This is a decrease when compared to 2020, however the period of market stress after the coronavirus shock, and subsequent volatility could have affected the ATV measure. This is based on observing abnormal increases in trading volumes in 238 out of 3364 announcements tested.

The existence of announcements where we have found statistically significant increases in volumes, does not mean that market abuse occurred before each of those announcements, as volumes can fluctuate for a variety of reasons, but it is an indicator that market abuse may have occurred.

Chart

Data table

Potentially Anomalous Trading Ratio (PATR)

We introduced the Potentially Anomalous Trading Ratio (PATR) as part of our work to broaden the number of indicators to help assess market cleanliness.

The new measure looks at potentially anomalous trading that occurs ahead of a price sensitive news announcement. By potentially anomalous trading we mean:

- the participant does not typically trade in this instrument

- the participant traded significantly more in the direction of the announcement

- the participant made a significant profit from trading positions established in the period immediately prior to the announcement

The PATR for 2021 was 6.1% which represents a small decrease from 6.9% in 2020.

It is important to understand this ratio in the context of the overall level of trading considered for this measure. Our analysis revealed 99.1% of trading activity did not occur during a sensitive time period (eg not preceding a potentially price sensitive news announcement where the price did move significantly). For the 0.9% of trading activity that justified further review, only 6.1% of that trading was considered potentially anomalous – a very small percentage of overall UK trading activity.

Chart

Data table